How metals and minerals will replace oil & gas as the world’s most valuable resources.

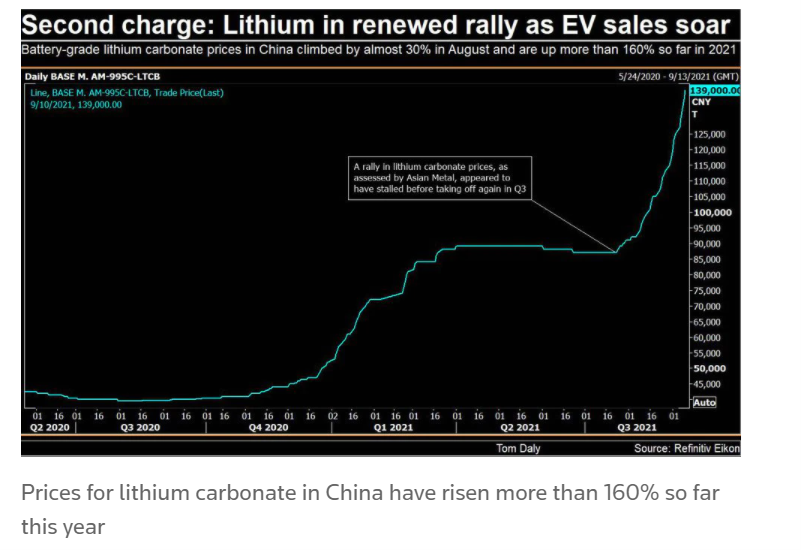

Why is the price of lithium soaring this year?

⛏️Why are the US Government backing a potentially highly polluting refining process in Texas and the Pentagon investigating so called biomining to secure supplies of rare earth metals?

📈Why is the demand for copper projected to rise rapidly in the next few decades?

The world economy is facing its biggest ever transformation as countries attempt to rapidly decarbonise in a bid to prevent runaway climate change. There will be a global energy transition from fossil fuels to renewable energy. This means solar and wind, but also hydrogen, geothermal and possibly nuclear all displacing oil, gas and coal.

Energy transition will bring in its wake huge shifts in geopolitical power. For many this transition will be painful. Many nations such as Saudi Arabia, Algeria and Norway will see the central pillar of their economy disappear along with it much of their power, influence and wealth. The countries that rapidly adopt new technology and adapt to this new world will emerge the winners.

Energy transition

⚡🛢️⛽Coal, oil, and natural gas remain the cornerstone of global energy. But change is happening, the global energy transition is well under way.

- Recent decarbonisation pledges from nearly every country in the world.

- The falling cost and efficiency of wind and solar power, plus the emergence of other alternatives such hydrogen means that a clean energy future is possible.

- Banks are turning away from fossil fuels as the long terms risks and costs become clear.

Energy transition means closing dirty coal fired power stations, refineries, and oil wells in favour of offshore wind farms, replacing petrol cars with electric and peppering roofs with solar panels.

Of course this change will be slower than many would like. The transition will be a bumpy ride, but it does now feel inevitable.

Rather than relying on physical inputs of coal, gas, and oil renewable energy is technology based. Solar panels with silicone cells, ever more efficient wind turbines and electric batteries.

Tech Competition

🔋China leads the race in terms of electric batteries. In 2021, 148 of the world’s 200 lithium-ion battery megafactories in the pipeline are located in China. Whereas Europe and North America have only 21 and 11 megafactories in the pipeline.

Electric batteries and the components for wind and solar require metals and minerals, from lithium, copper, cobalt, nickel, manganese and a host of rare earth metals. As the world scales up its use of clean energy demand for these materials will rise rapidly. Demand for lithium is expected to rise 40 fold by 2040 as the global energy transition accelerates.

The world will move from an energy intensive world to a mineral intensive one.

This fundamental change has massive consequences for mining, energy and geopolitics. The world can go from harvesting and processing 13 billion tonnes of fossil fuels a year to mining 43 million tonnes of critical minerals.

Currently the production of these critical materials is focused in just a few countries. Cobalt mining is 60 – 70 percent concentrated in China and the Democratic Republic of Congo (DRC). China dominates the dirty, polluting rare earth metal refining sector (90 percent of the market).

Rare Earth Materials

🪙Realising China’s dominance in the rare earth metals sector represents a major strategic weakness, forcing the US to react. US Presidential Executive Orders and the recent US$ 1 trillion infrastructure bill have identified and attempted to rectify these supply chain weaknesses. The government recently pledged US$ 30 million towards a rare earth refining facility in Texas. Other measures are sure to follow.

Tensions over mineral rights have surfaced in Greenland and Brazil where US and Chinese interests have clashed over the supply of minerals.

Any country that dominates the supply of critical materials can if it chooses cut or restrict the supply of materials. This would cripple the green tech industries of any opponents or rivals.

Global Competition

🌏Overseas the US and western allies are looking to secure supplies of critical metals and minerals. Countries from Kazakhstan, Mongolia, to Tanzania, Zimbabwe and Malawi all have potential for mining rare earth minerals. The competition between the US and China means that any potential location will be carefully vetted as a future geopolitical flashpoint.

South America and Lithium

🌎South America is also a rich source of lithium. The metal is in demand thanks to its use in electric car batteries. Mining companies have flocked to the so-called lithium triangle of Chile, Bolivia, and Argentina to secure mineral rights in the region. Large and relatively easy to reach deposits made the region a hotspot for both western and Chinese firms.

However, South American nations are not passive hosts. Resource nationalism will always raise its head to thanks to the decades of accusations of exploitation aimed at US firms. As lithium rises in value governments will more tempted to take more control over such an important asset.

Despite being a relative newcomer China is the biggest trade partner for many countries in South America. Chinese firms will compete hard against US or Western interests for mineral resources, particularly those which feed critical industries back home.

King Copper

⚡Copper is also essential for the global energy transition. In order to meet decarbonisation targets the world needs to electrify rapidly. Plugging growing energy demand into a renewable powered grid can decarbonise power sectors rapidly. An easy win for green targets. Electrification also means heavy use of copper for wiring.

No surprise then that copper demand is expected to rise by over the next decades. Wood Mackenzie estimates this will take US$130 billion to provide another 6.5 million tonnes per year. Major copper producers are already predicted to see falling market share.

The race is on to locate new sources to match future demand. The problem is that mining is a very slow drawn out process. The planning and development of any mining project can take years or decades until anything is actually produced.

Metal Heads

Geographical concentration of production could put lithium and other metals in the hands of just a few producers. This will give the miners and refiners significant monopoly power, potentially allowing them to control the supply and price of critical materials. In turn this will push up the cost of global energy transition.

Another big problem of concentration is that any disruption through conflict, trade disputes and increasingly extreme weather events could disrupt the flow of metals to factories. Any disruption has a knock on effect delaying global energy transition.

Dirty Dangerous and Difficult

🌲Global energy transition is supposed to be environmentally friendly. Cutting out fossil fuels from the global energy mix will be decarbonise the sector, but what about other environmental factors? Unfortunately, mining is a notoriously polluting sector.

Monitoring and measuring the sustainability of supply chains and mines will come under ever greater scrutiny. The pollution and human cost of refining rare earth metals is one reason countries have not flocked to host these facilities. Inner Mongolia in China is host to huge toxic lakes full of black sludge, the by-products of rare earth metal refining.

Manufacturers of green tech do not want their credentials undermined by dirty polluting mines that abuse labour. This should put pressure on miners to clean up their act, but this could also push up the cost of extraction. However. these constraints will also spur innovation.

Recycling the electrical revolution

Recycling electric batteries, wind turbines and electrical goods has become an industry in itself as entrepreneurs try to salvage the most valuable parts of clean energy technology. An industry that is pushing sustainability does not want a dirty underbelly of waste.

At the same time demand for transition metals and minerals will push mining companies to look for new sources in different regions. This will lead to a hunt for metals and minerals that feed the energy transition that will be complicated by geopolitical competition.

Geopolitics of global energy transition

🌏The geopolitics of a mineral intense world will also look very different.

Firstly, marginal oil producers where production is expensive are likely to go out of business first when oil demand finally wanes. Places like Venezuela where the cost of production is high and the quality of oil low will be first to go and along with it any oil based geopolitical leverage.

Supply chain disruptions will not be severe as seesawing oil demand. A tight lithium supply will only impact building new electric batteries not existing vehicles. Oil requires near constant supplies to avoid disruption.

Shifting countries away from being petro-states will help them in the long run. Oil often poisons the politics of a country and creates a parasitic mono-economy.

Saudi Arabia and Gulf states will retain their power the longest. The cost of production in this region is much lower, so oil production can be sustained for longer.

What comes next?

What will replace the era of fossil fuel geopolitics. Countries that control the mining and refining of critical minerals such as lithium, cobalt and copper will gain newfound power in the energy transition. Rocketing demand and concentration of supply will create lots of talk about the “Saudi Arabia’s of lithium”.

The shift to a mineral intensive world will hand greater power to the countries and companies that can control the supply and processing of critical minerals and metals. The rest of the world will be keen to ensure that there are reliable supplies of critical materials to ensure a smooth transition.

Key Takeaways:

- Demand for the raw materials that will build a climate economy: Copper, cobalt, lithium, graphite and rare earth metals will enjoy unprecedented demand over the coming decades. More solar panels, electric batteries and electrification means more mining for critical materials and less fossil fuels.

- Mining is a dirty business. There will be major opportunities to help mining companies improve their environmental and social performance.

- There is a risk that a lack of or the high cost of raw materials such as copper will stop the world from hitting decarbonisation targets. Copper projects can take years to become productive.

- Demand for metals such as lithium combined with falling demand for oil and gas will shift global geopolitics. Lithium producers will enjoy greater bargaining power as China and western countries compete over supplies. Key oil producers such as the Gulf States will see their power grow in the medium term as marginal oil producers are forced out of business as demand falls.